Comprehending the Basics of Protecting a Mortgage for Your New Home

Beginning on the journey to safeguard a home loan for your new home requires a comprehensive grip of numerous fundamental aspects. The selection of mortgage types, subtleties of rates of interest, and the essential role of credit rating all add to the complexity of this procedure. As you navigate the myriad of alternatives and demands, understanding exactly how these components interplay can be essential to your success. What genuinely empowers prospective property owners is often ignored. Could there be an essential technique that simplifies this relatively challenging venture? Let's discover just how to properly approach this vital monetary choice.

Types of Mortgage Loans

Navigating the varied landscape of home loan is crucial for potential homeowners to make educated financial decisions - mortgage loan officer california. Recognizing the different kinds of mortgage available can significantly impact one's choice, lining up with economic goals and personal circumstances. The most typical kinds consist of fixed-rate, adjustable-rate, FHA, VA, and big loans, each serving unique demands

For people with restricted down payment capabilities, Federal Housing Administration (FHA) finances supply a sensible option, calling for reduced down repayments and credit history. Veterans and active-duty armed forces members could receive VA financings, which offer affordable terms and typically require no deposit. Lastly, jumbo lendings satisfy purchasers in high-cost locations looking for to fund properties surpassing standard financing limits.

Choosing the ideal mortgage kind includes examining one's financial stability, future plans, and convenience with threat, making certain a well-suited pathway to homeownership.

Recognizing Rates Of Interest

Realizing the subtleties of interest prices is necessary for anyone considering a home mortgage, as they directly affect the overall price of borrowing. Interest rates establish just how much you will certainly pay along with settling the principal quantity on your home loan. Hence, recognizing the distinction in between fixed and variable rate of interest is critical. A set rate of interest continues to be continuous throughout the funding term, offering predictability and security in regular monthly settlements. In contrast, a variable or adjustable-rate home mortgage (ARM) might start with a reduced rate of interest rate, but it can fluctuate gradually based on market problems, possibly enhancing your payments considerably.

Passion rates are largely influenced by financial elements, including inflation, the Federal Book's financial plan, and market competition amongst lenders. Debtors' credit rating ratings and economic profiles likewise play an essential role; greater credit rating ratings generally secure reduced rates of interest, mirroring decreased danger to loan providers. Because of this, improving your credit report prior to getting a mortgage can cause substantial savings.

It's critical to compare offers from multiple lenders to guarantee you secure the most favorable rate. Each percentage over here point can impact the long-lasting price of your mortgage, emphasizing the value of extensive study and educated decision-making.

Financing Terms Clarified

A crucial element in understanding home loan arrangements is the car loan term, which dictates the period over which the borrower will pay back the financing. Typically expressed in years, car loan terms can dramatically affect both month-to-month payments and the total passion paid over the life of the lending. One of the most typical home loan terms are 15-year and 30-year durations, each with unique advantages and considerations.

A 30-year financing term permits lower monthly payments, making it an attractive choice for lots of homebuyers looking for price. However, this extensive settlement duration typically results in greater overall passion prices. Conversely, a 15-year car loan term generally includes higher month-to-month repayments however provides the advantage of decreased passion amassing, allowing house owners to build equity quicker.

It is vital for consumers to examine their financial circumstance, lasting objectives, and danger tolerance when picking a funding term. Furthermore, comprehending other variables such as prepayment charges and the potential for refinancing can offer more flexibility within the picked term. By carefully considering these components, debtors can make enlightened choices that line up with their monetary objectives and make certain a manageable and successful home loan experience.

Value of Credit Rating

Having a great credit history can dramatically affect the terms of a home mortgage financing. Debtors with higher scores are generally supplied reduced rates of interest, which can bring about substantial savings over the life of the funding. Additionally, a solid credit report score might increase the probability of lending authorization and can provide higher negotiating my explanation power when discussing finance terms with lenders.

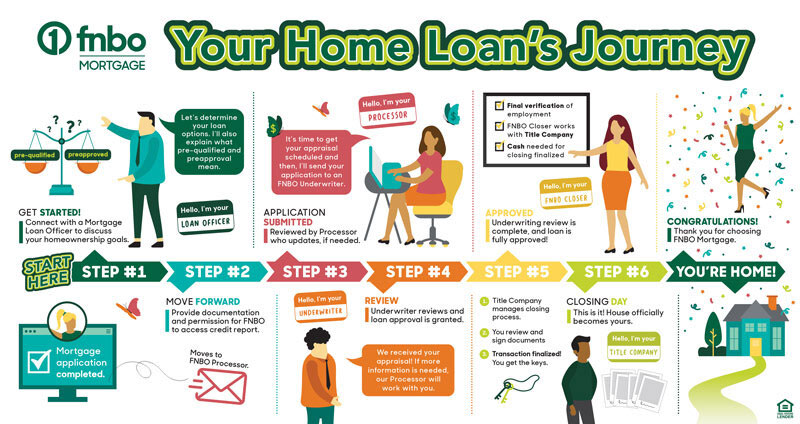

Browsing the Application Process

While credit report play an essential duty in safeguarding a home loan, the application procedure itself calls for careful navigating to ensure a successful end result. The process starts with collecting necessary documentation, such as proof of earnings, tax obligation returns, financial institution declarations, and identification. This documentation gives lenders with a detailed view of your economic security and capacity to repay the finance.

Following, study various loan providers to compare rate of interest, lending terms, and fees. This step is crucial, as it aids recognize one of the most positive home loan terms tailored to your financial scenario. As soon as you have actually chosen a lender, finishing a pre-approval application is suggested. Pre-approval not just enhances your negotiating power with sellers yet additionally supplies an accurate image of your loaning ability.

Throughout the home loan application, ensure precision and completeness in every information provided. Errors can result in hold-ups or also denial of the application. In addition, be prepared for the lending institution to request more info or clarification throughout the underwriting process.

Conclusion

Securing a mortgage finance requires a comprehensive understanding of various elements, consisting of the kinds of loans, interest prices, lending terms, and the function of credit scores. Reliable navigation of these aspects is necessary for an effective mortgage application process.

Comments on “Understanding the Role of a Mortgage Loan Officer California in Securing Your Dream Home”